Next-Gen Indian Digital Banking

AEPS • Money Transfer • BBPS • Recharge • UPI — Fast, Secure & Trusted Fintech Platform.

Banking Services

Powerful fintech services designed for Indian retailers & customers.

AEPS

Cash withdrawal, balance enquiry & mini statement using Aadhaar authentication.

Money Transfer

Instant IMPS/NEFT transfer to any Indian bank with high success rate.

Recharge

Mobile, DTH & data card recharge for all operators across India.

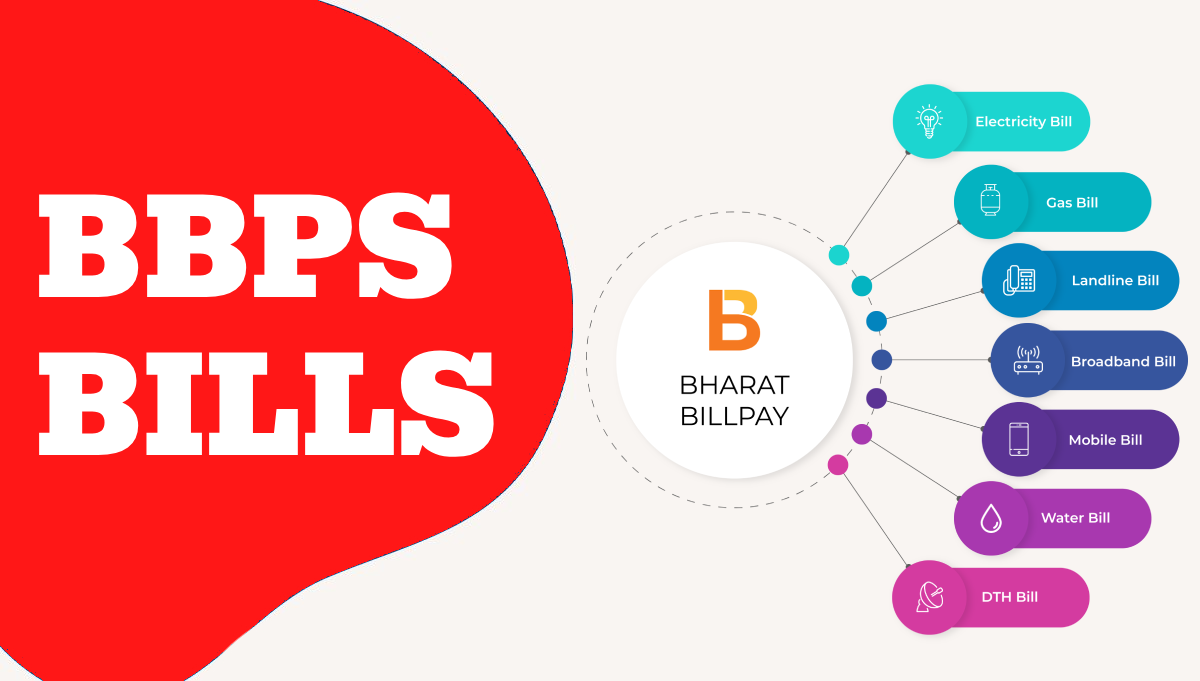

BBPS Bills

Electricity, gas, water & FASTag payments with instant confirmation.

UPI QR

Collect payments instantly via dynamic QR & UPI ID integration.

PAN & KYC

Instant PAN services & Aadhaar based digital KYC verification.

10K+

Active Retailers

1M+

Transactions Monthly

99.9%

Success Rate

Grow Your Fintech Business Today

Join India's fastest growing digital banking service platform. Contact Us

All‑in‑One Digital Banking Platform

Provide seamless AEPS, money transfer, BBPS bill payment, recharge, UPI collection, and KYC services through a single secure fintech dashboard designed for Indian retailers and distributors.

- ✔ Instant settlements & real‑time transaction tracking

- ✔ Secure Aadhaar‑based authentication

- ✔ High success rate with smart routing

- ✔ Dedicated retailer support system

How It Works

Start your digital banking journey in simple steps.

1

Register

Create your retailer account in minutes.

2

Complete KYC

Verify Aadhaar & PAN for activation.

3

Add Balance

Load wallet securely via bank transfer.

4

Start Earning

Provide banking services & earn commission.

Frequently Asked Questions

Everything you need to know about our fintech services.

Retailers can offer AEPS cash withdrawal, money transfer, bill payments, mobile recharge, UPI collection,

and KYC services from a single dashboard.

Account activation usually completes within a few hours after successful KYC verification.

Yes, we use encrypted APIs, Aadhaar authentication, and secure banking infrastructure to protect

all transactions and user data.